Retirement Planner in Vermont, Victoria: Your Guide to a Financially Secure Retirement

Retirement is one of the most significant financial milestones in life. Whether you’re approaching retirement, transitioning out of the workforce, or already retired, working with a professional retirement planner in Vermont can help you make informed decisions about your financial future.

Many Australians underestimate how much money they will need in retirement. Factors such as increasing life expectancy, inflation, healthcare costs, and market volatility can significantly impact retirement outcomes. A well-structured retirement plan helps ensure you have the financial resources needed to maintain your desired lifestyle throughout retirement.

This guide explains how retirement planning works, why it matters, and how a retirement planner in Vermont, Victoria can help you achieve long-term financial security.

Retirement planning isn't about stopping work - it's about creating the freedom to live life on your terms.

What Does a Retirement Planner in Vermont Do?

A retirement planner helps individuals develop strategies to achieve financial independence during retirement. Their role involves analysing current finances, forecasting future needs, and creating tailored retirement plans.

Retirement Goal Setting

Every retirement plan starts with understanding your goals.

Examples include:

- Desired retirement age

- Expected lifestyle expenses

- Travel plans

- Supporting family members

- Leaving a financial legacy

Retirement Income Planning

One of the biggest retirement concerns is ensuring income lasts throughout retirement.

A retirement planner can help structure:

- Superannuation withdrawals

- Pension income streams

- Investment income

- Cash reserves

Superannuation Strategies

Superannuation often forms the foundation of retirement wealth.

A retirement planner may assist with:

- Contribution strategies

- Investment allocation

- Consolidation of accounts

- Retirement phase planning

Why Retirement Planning is Important

Increasing Life Expectancy

Australians are living longer than previous generations. A retirement that lasts 20–30 years requires careful financial planning.

Rising Cost of Living

Inflation can gradually reduce purchasing power over time.

Retirement plans should account for:

- Housing costs

- Utilities

- Insurance

- Daily living expenses

Healthcare and Aged Care Considerations

Healthcare costs often increase later in life.

Planning ahead can help cover:

- Medical expenses

- Residential aged care

- Home care services

- Specialist healthcare requirements

Key Components of aSuccessful Retirement Plan

Superannuation Planning

Superannuation remains one of Australia’s most tax-effective retirement savings vehicles.

Common strategies include:

- Salary sacrifice contributions

- Personal deductible contributions

- Spouse contributions

- Contribution caps management

Investment Strategies

Retirement investments should balance growth, income, and risk.

| Investment Type | Primary Purpose |

|---|---|

| Shares | Long-term growth |

| ETFs | Diversification |

| Managed Funds | Professional management |

| Property | Asset growth |

| Fixed Interest | Income stability |

| Cash | Liquidity |

Pension and Centrelink Considerations

Government benefits can form part of retirement income planning.

Areas to consider:

- Age Pension eligibility

- Income tests

- Asset tests

- Pension supplements

Estate Planning

Estate planning ensures assets are distributed according to your wishes.

Key documents include:

- Will

- Power of Attorney

- Binding Death Benefit Nominations

- Testamentary Trusts

Retirement Planning Strategies for Vermont Residents

Pre-Retirement Planning

The years leading up to retirement provide opportunities to strengthen retirement readiness.

Important actions include:

- Increasing superannuation contributions

- Reducing debt

- Reviewing investments

- Assessing retirement income needs

Transition to Retirement Strategies

Transition to Retirement (TTR) strategies may help eligible individuals improve retirement outcomes while still working.

Potential benefits include:

- Tax efficiencies

- Increased superannuation balances

- Flexible work arrangements

Post-Retirement Wealth Management

Retirement planning does not end once retirement begins.

Regular reviews help ensure:

- Income remains sustainable

- Investments remain appropriate

- Financial goals stay on track

Why Choose Future Needs Retirement Planners in Vermont?

At Future Needs Financial Services, we understand that retirement means different things to different people. Our goal is to help you retire with confidence through personalised financial advice and long-term planning strategies.

Personalised Retirement Advice

We take time to understand your:

- Retirement goals

- Lifestyle expectations

- Financial position

- Risk tolerance

This allows us to create tailored retirement strategies aligned with your needs.

Comprehensive Retirement Planning Services

Our retirement planning solutions include:

- Retirement Income Planning

- Superannuation Advice

- Pension Planning

- Investment Management

- Wealth Protection Strategies

- Estate Planning Support

Ongoing Retirement Reviews

Retirement plans should evolve as circumstances change.

We provide:

- Regular strategy reviews

- Investment monitoring

- Retirement income assessments

- Legislative updates and guidance

Local Expertise You Can Trust

Serving Vermont and Melbourne’s eastern suburbs, we understand the unique financial needs of retirees, pre-retirees, professionals, and families seeking retirement security.

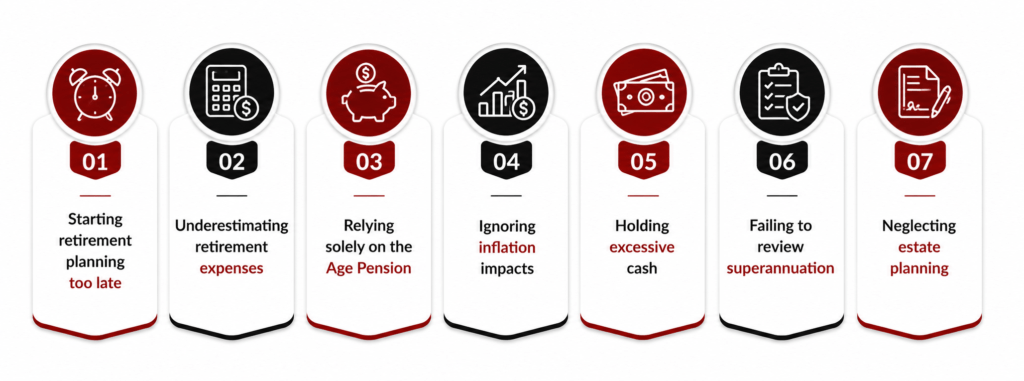

Common Retirement Planning Mistakes Mistakes

FREQUENTLY ASKED QUESTIONS

A retirement planner helps individuals create strategies for retirement income, superannuation, investments, pensions, and wealth preservation.

Ideally, retirement planning should begin as early as possible, but it’s never too late to improve retirement outcomes.

The amount varies depending on lifestyle expectations, retirement age, and personal circumstances.

Yes. Superannuation optimisation is a key component of retirement planning.

At least annually, or whenever major life changes occur.

Superannuation often forms the foundation of retirement income strategies in Australia.

Yes. Retirement planners can help assess Age Pension eligibility and retirement income strategies.

No. Retirement planning also involves investments, pensions, estate planning, tax strategies, and wealth management.

Future Needs provides personalised retirement planning, superannuation advice, investment strategies, and ongoing support tailored to your goals.